Digital banking is entering a new phase.

The next breakthrough is not another cleaner app menu, another dashboard, or another chatbot that only answers FAQs. The next banking experience is conversational, intelligent, and action-oriented.

Imagine a customer typing:

Send RM50 to Sarah for lunch.

Or uploading a bill and saying:

Pay this before Friday.

Or taking a photo of a dinner receipt and asking:

Split this with Amir, Mei Ling, and Daniel.

This is the future of AI banking: customers express intent in natural language, and the banking platform understands, validates, prepares, and executes the transaction securely with user confirmation.

Agmo helps banks, digital banks, fintechs, e-wallets, and financial institutions design and build AI-native banking experiences that turn everyday financial tasks into simple conversations.

Most banking apps are still built around menu navigation. Customers need to know where to tap, which feature to open, which biller category to choose, and which reference number to copy.

AI changes that.

Instead of forcing users to follow the bank’s interface, the bank can now understand the user’s intent.

This creates a major opportunity for financial institutions to:

For CTOs and CIOs, this is not just a UX upgrade. It is a new interaction layer for banking.

Customers can send money using normal language instead of navigating through multiple screens.

Example user prompts:

Send RM100 to Farah for dinner.

Transfer RM500 to my Maybank savings account.

Pay back Jason RM38 for Grab.

The AI banking assistant can understand the amount, recipient, payment purpose, account source, and transaction type. It then prepares the transfer and asks the user to review and confirm before execution.

This makes banking feel like messaging, while keeping the transaction flow controlled, validated, and secure.

Bill splitting is one of the most natural AI banking use cases.

A user uploads a restaurant receipt, and the AI assistant can:

Example prompt:

Split this nasi lemak lunch receipt equally with Aisyah, Kumar, and Ben.

For younger customers, families, office groups, and social spenders, this becomes a high-frequency engagement feature inside the banking app.

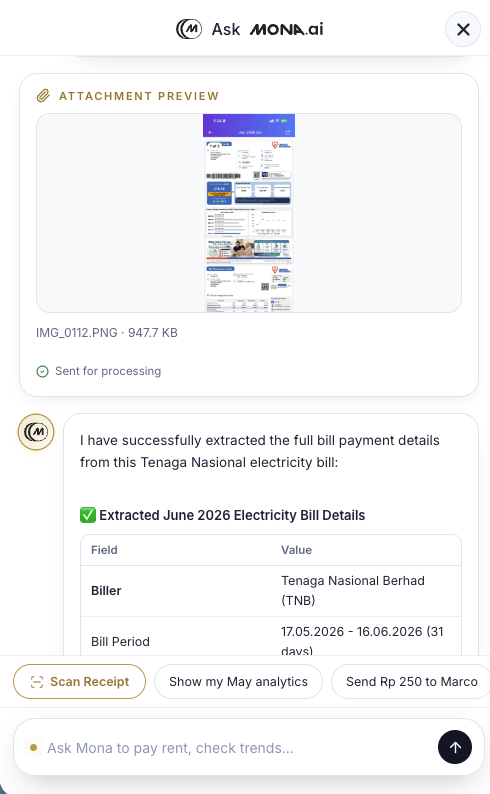

Paying bills is still too manual.

Customers often need to copy biller codes, account numbers, reference numbers, and amounts across PDFs, screenshots, emails, or paper bills.

With AI banking, the user simply uploads a bill.

The assistant can detect:

Example prompt:

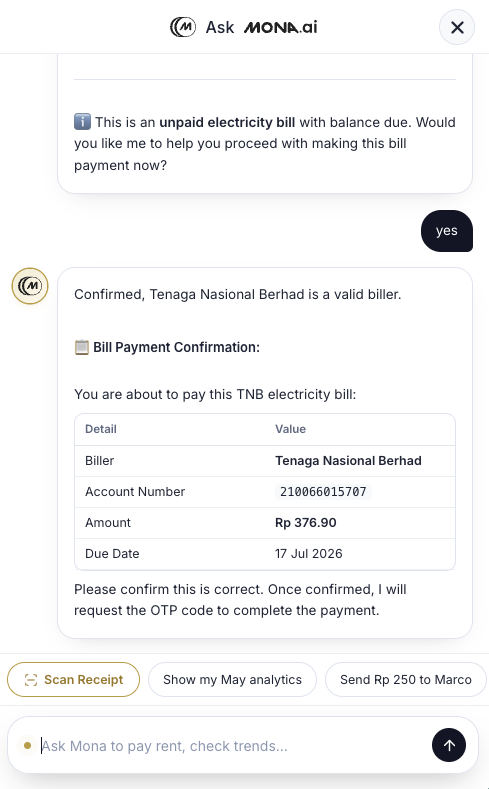

Pay this electricity bill from my main account.

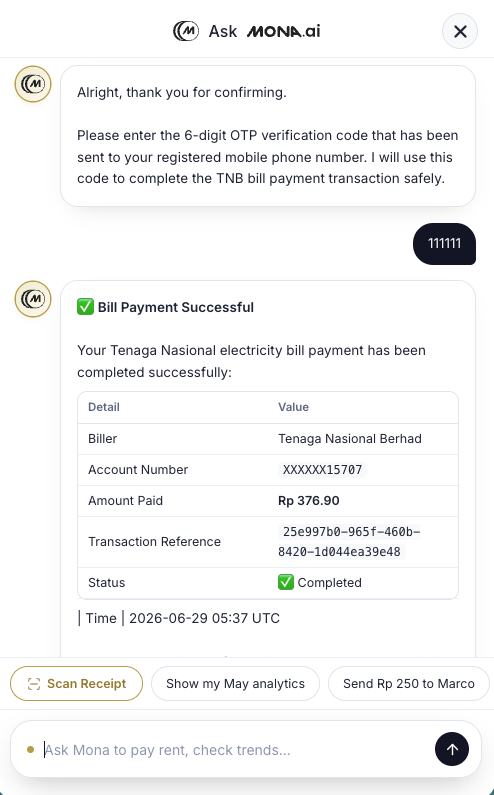

The AI assistant extracts the payment details, maps the biller, prepares the transaction, and presents a confirmation screen before payment.

This reduces user error, improves bill payment conversion, and makes digital banking more useful for everyday life.

Instead of forcing users to read charts, AI banking lets users ask financial questions naturally.

Example prompts:

How much did I spend on food this month?

Show me my top 5 spending categories.

Why is my spending higher than last month?

How much did I pay for subscriptions this year?

The AI assistant can turn transaction history into plain-language insight, helping customers understand their money without manually filtering statements.

This is especially powerful for personal finance management, savings nudges, budget tracking, and financial literacy.

Customers often ask the same questions:

What is my transfer limit?

How do I increase my card limit?

Which account gives better savings returns?

What documents do I need for this application?

Instead of generic FAQ search, the AI assistant can retrieve answers from approved bank knowledge sources and provide guided explanations.

For banks, this reduces support load. For customers, it creates a more human, accessible banking experience.

The AI layer can sit above existing payment rails and banking services.

Potential integrations include:

The key is not replacing the payment infrastructure. The key is creating an intelligent front layer that understands intent and orchestrates the correct banking workflow.

AI banking must be built differently from a normal chatbot.

A banking AI assistant cannot simply generate answers freely. It must be engineered with strong control, deterministic validation, and auditable transaction flow.

Agmo’s AI banking architecture typically includes the following layers.

The assistant identifies what the customer is trying to do:

This layer converts natural language into structured banking intent.

For uploaded receipts, bills, screenshots, or PDFs, the system extracts structured information such as:

This enables bill payment, receipt splitting, reimbursement, claims, and transaction matching.

For FAQs, product rules, policies, interest rates, terms, and support content, the assistant should answer using approved bank knowledge only.

A Retrieval-Augmented Generation layer can be implemented so the AI retrieves from:

This improves consistency, reduces hallucination risk, and gives the bank better control over responses.

The AI assistant prepares the transaction but does not bypass banking controls.

The payment orchestration layer maps the user intent into the right workflow:

It validates mandatory fields, handles missing information, and prepares the transaction for confirmation.

For banks, safety is non-negotiable.

The AI assistant must include controls such as:

The AI can assist. The deterministic banking system must still validate and approve.

Agmo can integrate the AI experience with the bank’s existing ecosystem:

This ensures the AI banking experience is not a standalone gimmick, but part of the real banking stack.

Every AI banking interaction should be traceable.

The platform should capture:

This gives CTO, CIO, risk, compliance, and audit teams the visibility needed to run AI safely in a regulated environment.

Send RM80 to Daniel for dinner.

The assistant prepares a transfer and asks for confirmation.

User uploads a TNB, water, telco, or assessment bill.

The assistant extracts details and prepares bill payment.

User uploads a receipt.

The assistant splits equally or by item and generates payment requests.

How much did I spend on petrol this month?

The assistant analyses transaction categories and gives a plain-language answer.

Remind me to pay this bill 3 days before due date.

The assistant creates a reminder or scheduled workflow.

What is the daily transfer limit for my account?

The assistant answers using approved bank documents.

The AI assistant answers common support questions and escalates complex cases to human agents.

AI banking is moving from novelty to customer expectation.

Banks that act early can build:

The winning banks will not simply add AI to the app. They will redesign banking around intent.

Agmo brings the full capability required to build AI banking platforms:

We can support banks and fintechs through different engagement models:

Whether you want to build a full AI-native banking experience or start with one focused use case, Agmo can help you design, implement, integrate, and scale it.

The best way to start is not to rebuild the whole banking app.

Start with one high-frequency, low-risk, measurable workflow:

Within a pilot, we can define:

If you are planning the next generation of digital banking, now is the time to explore AI-native banking experiences.

Agmo can help you build a conversational banking layer that allows customers to send money, pay bills, split receipts, understand spending, and interact with banking services using natural language.

Talk to us to design your AI banking pilot.

Let’s turn your banking app from a menu-based interface into an intelligent financial assistant by writing to us at [email protected]